VC-Backable TAM in Healthtech: Challengers and Enablers

As Marc talks about here (~5:17), one of the biggest unlocks in VC-backed tech was when companies started going full stack to challenge incumbents head-on ("Challengers"), versus just building tools for incumbents ("Enablers"). This evolution didn't diminish the value contribution of Enablers - for every AirBNB, Uber, and SpaceX, there is a Stripe, Databricks, and Nvidia. The expansion of VC-backable TAM over the last couple of decades was driven explicitly by the combination of both.

For VC-backed healthtech to have staying power, we'll need the same thing to happen - both Enablers (e.g. RCM, practice management, EHR, interoperability, AI automation systems, etc) and Challengers (e.g. insurance companies, medical services companies, pharmacies, etc) will be needed to drive the creation of attractive and sustainable levels of VC-backable healthtech TAM.

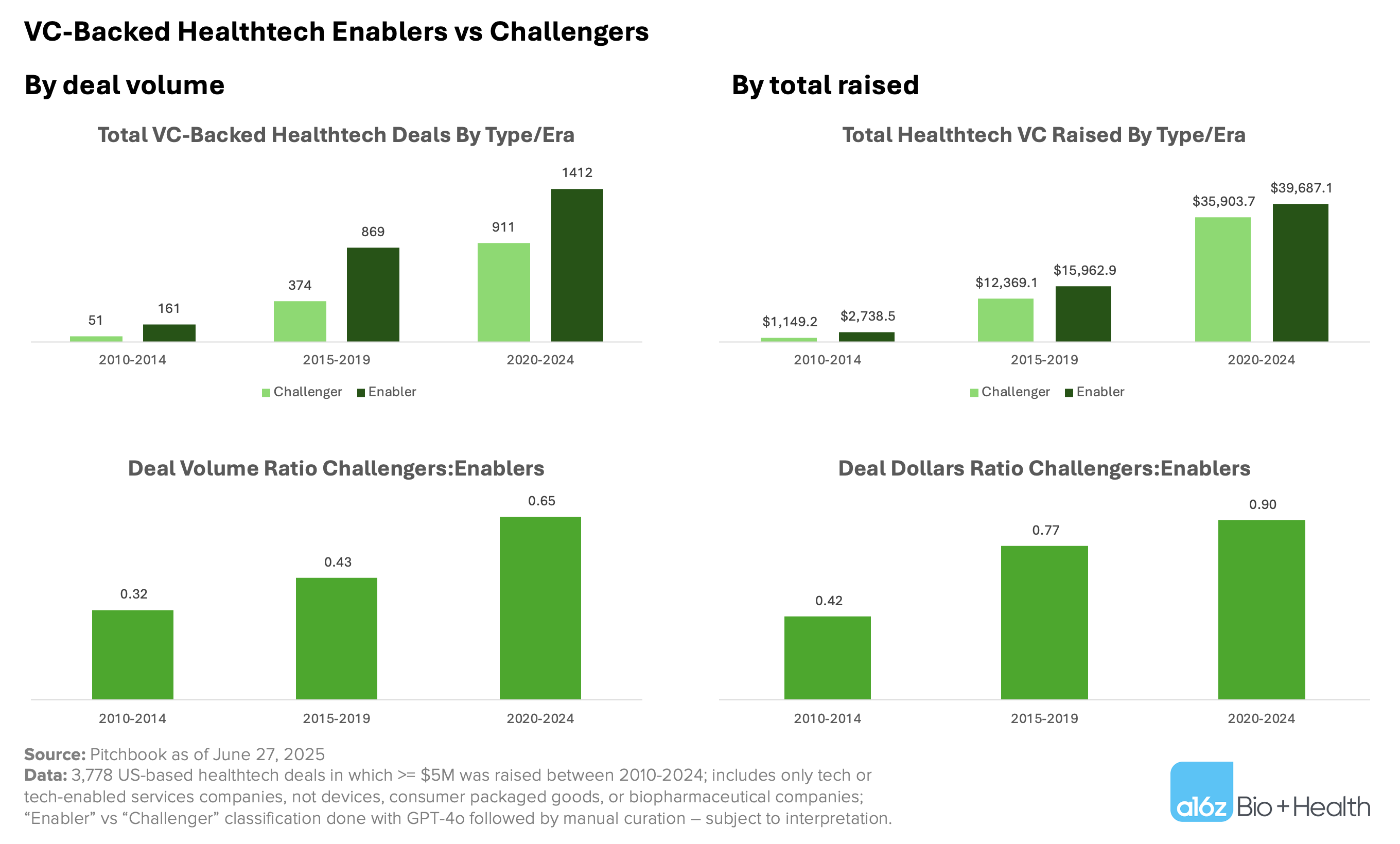

Looking at VC healthtech funding trends from the last 15 years, we’ve actually seen this play out - Enablers have dominated in terms of overall volume of deals, but the ratio of VC deals into Challengers versus Enablers has risen from 0.32:1 between 2010-2014 to 0.65:1 in 2020-2024. The ratio of total dollars raised by Challengers versus Enablers has also more than doubled, from 0.42:1 in 2010-2014 to 0.90:1 in 2020-2024:

While the fundraising data above imply that Challengers are just starting to catch up with Enablers, public healthtech listings in the last 15 years (either IPO or SPAC) show that Challengers just pulled ahead in terms of volume - 11 out of 21 VC-backed public market entrants between 2020 and 2024 were Challengers. In terms of aggregate peak first-year market cap, Challengers trailed Enablers in each era to date - though given the small total <n>, a small number of outlier numbers swayed these metrics (link to raw data at bottom).

So what does this mean for healthtech founders?

For Challengers:

A common trope is that it’s harder to raise capital as a Challenger versus as an Enabler, since Challengers tend to be more capital-intensive, with lower margin profiles than Enablers. Also, since most revenue in healthcare is reimbursed through third-party payors or government, even the most full-stack-iest Challengers may rely on contracts with incumbents for a non-trivial portion of their revenue, which could cap their upside (i.e. the revenue cycle management “tax”), or at a minimum slow them down.

But the analyses here indicate that Challengers are increasingly raising just as much private capital as Enablers, and may represent a larger proportion of healthtech companies that ultimately go public over time. The rise of AI products being used as labor substitutes (with margins that are superior to traditional tech-enabled services companies) will likely also contribute to increasing amounts of capital deployment into, and value creation through, AI-native Challenger models.

(We should note that a non-trivial number of publicly-traded Challengers ended up declaring bankruptcy (5), which could imply that it’s harder for these players to stay afloat in the public markets than Enablers - perhaps because of business model quality and/or scalability issues. See raw data for specific examples.)

For Enablers:

Enablers appear to be attracting funding at a steady clip, but have comprised a smaller share of recent public listings than Challengers. We talked here about the inherently high degree of customer concentration for enterprise healthcare companies, which could be an inhibitor to growth for Enablers. But the Enablers that do figure out how to capture large ACVs per customer (e.g. Veeva) and/or sell into multiple segments of the healthcare industry (e.g. Tempus, Doximity) can get just as big as Challengers, with the benefit of being valued using tech versus services multiples.

Some Enablers may be compelled to vertically integrate into Challengers over time to capture more value and/or take more premium dollar risk, e.g. Accolade acquiring PlushCare to become a care provider, or AmWell starting as a tech platform before vertically integrating into a telehealth services provider.

Finally, agentic AI will continue to drive growth in this category of the market as well - AI-native scribes and RCM automation companies have already generated $100M’s in ARR in just the past couple of years alone, and AI is eating into a broad surface area of other fast-growing Enabler modalities.

—

These fundraising and public listing trends indicate that whereas the majority of the initial cohort of healthtech startups began as “picks and shovels” Enabler companies, Challengers have been increasingly contributing to the growth of VC-backable healthtech TAM, just as we saw in generalist tech. The massive waves of value creation we’ve experienced in the broader tech industry occurred over 4+ decades - and it’s still growing at rates most market participants could not have predicted in years past - so if healthtech follows suit in a manner that is anywhere close to how tech has played out, then we’re likely still very much in the early days of VC-backable TAM expansion in healthtech.

Raw data available here; welcome any feedback on the classification of Challengers vs Enablers (and acknowledge that some companies could be both or may have evolved over time).